Customs Duty- Ad Valorem and Excise

Customs Duty is payable to HM Customs immediately upon import of goods and is non-refundable, except in certain special circumstances. It is a tax on the importation of goods.

Duty is usually, though not always, calculated as a percentage of the “landed” value of the goods, in other words the value of the goods once the cost of their shipment to the UK has been taken into account.

A typical calculation for Customs Duty would comprise:

Value of goods + Freight Costs + Any Insurance cost X Duty percentage rate =

In certain instances Duty is payable on quantity of items rather than value. There may also be additional duties to pay on particular types of goods, for example foods or wine. Some of these Duties are known as Excise. As with Ad Valorem Duty it is payable on import, is non refundable and is most often payable in addition to Ad Valorem Duty.

Duty rates can vary considerably from just one or two percent to over fourteen percent. Many items also carry a nil rate. It is therefore essential that the correct classification code be obtained.

VAT (Value Added Tax)

VAT is a tax payable to HM Customs immediately upon the import of virtually all goods brought into the UK. VAT is payable on the landed cost of the goods plus Duty and clearance charges. Customs dictate the declaration of a nominal amount for the clearance charges. On airfreight this is £100.00 or £0.40 per kilo.

A typical calculation for Import VAT would comprise:

Value of goods + Freight Costs + Insurance + Duty + Clearance Costs X VAT rate = VAT

If you are registered for VAT you are able to reclaim all VAT paid on import, this is done in conjunction with your usual VAT returns (C79).

If you are not registered you will not be able to reclaim, but you must register with HM Customs prior to arrival of the goods. They will issue a number which can be used on initial and subsequent Customs entries and which can be used by you to reclaim the VAT paid if and when you do decide to register

All product imported into the UK must be classified using the Customs Tariff. The classification code, sometimes known as Commodity Code, Tariff Heading or Harmonised Code is the key to discovering what Duty rates, restrictions and reliefs may apply to the import of your goods.

- Duty rates can vary considerably from just one or two percent to over fourteen percent. Many items also carry a nil rate.

- From certain countries relief from Duty may be available upon production of the correct certificate.

- Some items are subject to import licence requirements

- Some items are subject to documentary requirements such as Certificate of Origin

It is absolutely vital to ensure that you have obtained the correct Commodity code for your goods prior to completing any order. If the code indicates that goods are subject to an Import Licence or that you may be able to obtain relief from Duties it is important that you and your supplier are aware of the attendant documentary requirements as certain certificates may not be available once consignments have departed the country of origin.

Customs Duty- Ad Valorem and Excise

Once you are satisfied that your goods are correctly classified you should check that the Customs Procedure to be utilised is suitable

If you are importing goods for any other purpose than to sell them within the EU you may be able to claim relief from Duty and / or VAT.

For example goods being imported for repair you can utilise a Customs Procedure known as Inward Processing Relief, under which full relief can be obtained.

There are a great number of Customs Procedures; again it is important to make yourself aware of what is available and suitable prior to shipment.

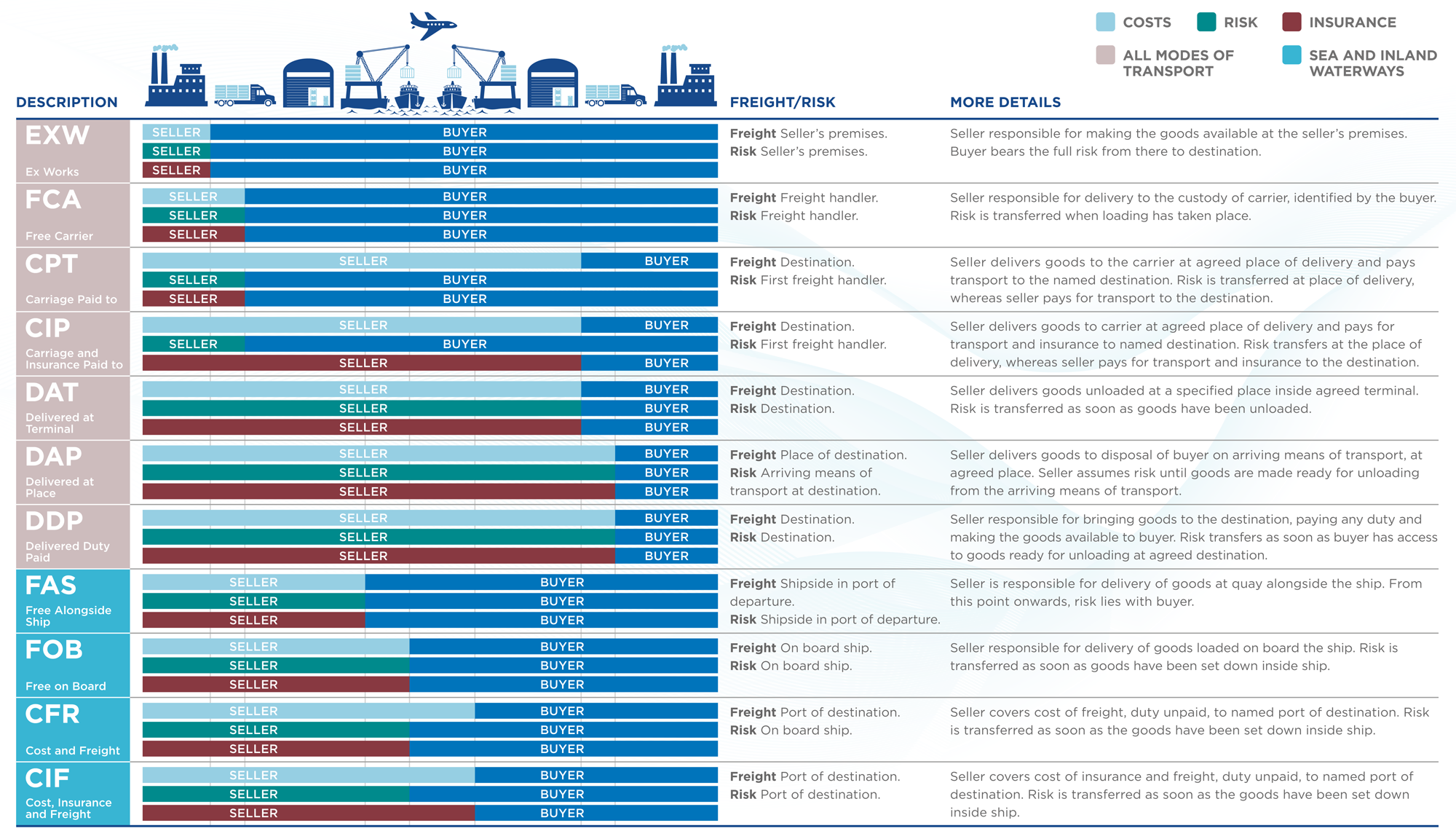

The Incoterms or Shipping terms will be the agreed purchasing terms and conditions between a supplier (consignor) and their client (consignee). It is the incoterm which sets the parameters for a financial transaction and specifies which costs becomes the responsibility of the parties involved.

The incoterms can significantly affect the overall cost and handling of the imported product, it is therefore essential you know your options prior to any agreement and have a clear understanding of the benefits of choosing the right incoterm for your import requirements.

The most commonly used ‘Incoterm’ are as follows:

DDP – Delivered Duty Paid: The supplier pays ALL charges for transporting the consignment to your door. (This will exclude in most cases VAT as this can be reclaimed by the consignee)

DDU – Delivered Duty Unpaid: The supplier pays all charges for transporting the consignment to your door, except any import Duty and/or VAT.

CIF – Cost Insurance Freight: The supplier pays all charges for transporting the consignment the UK. The value of the goods shown on the invoice/bill of sale includes these costs. All UK charges are for your account

C&F – Cost & Freight: This is the same as above, but in the shipper has not paid for any insurance.

FOB – Free On Board: The supplier pays for the goods to be transported to the port/ airport of departure. All other charges are for your account.

EXW – Ex Works. You pay all charges incurred from supplier’s door to your own.

| EQUIPMENT | INTERIOR DIMENSIONS | DOOR OPENING | TOP OPENING | TARE WEIGHT | CUBC CAPACITY | PAYLOAD |

|---|---|---|---|---|---|---|

| 40′ High cube Container | L:12.056m 39′ 6 ½ W:2.347m 7′ 8 ¼ H:2.684m 8′ 5½ | W:2.340m 7’8 H:2.585m 8′ 5 ¾ | 2,900 kg 6,393 lbs | 76.0 cbm. 2,684 cu. ft. | 29,600 kg 62,256 lbs. | |

| 40′ Dry Container | L:12.051m 39′ 6 ½” W:2.340m 7′ 8″ H:2.380m 7′ 9½” | W:2.286m 7′ 6″ H:2.278m 7′ 5 ½” | 3,084 kg 6,799 lbs. | 67.3 cbm. 2,377 cu. ft. | 27,397 kg 60,401 lbs. | |

| 20′ Dry Container | L:5.919m 19′ 5″ W:2.340m 7′ 8″ H:2.380m 7′ 9 ½” | W:2.286m 7′ 6″ H:2.278m 7′ 5 ½” | 1,900 kg 4,189 lbs. | 33.0 cbm 1,116 cu. ft. | 22,100 kg 48,721 lbs | |

| 20′ Open Top Container | L:5.919m 19′ 5″ W:2.340m 7′ 8″ H:2.286m 7′ 6″ | W:2.286m 7′ 6″ H:2.251m 7′ 4 ½” | L:5.425m 17′ 9 ½” W:2.222m 7′ 3 ½” | 2,174 kg 4,793 lbs | 31.6 cbm. 1.116 cu. ft. | 21,826 kg 48,117 lbs |

| 40′ Open Top Container | L:12.403m 39′ 6″ W:2.338m 7′ 8″ H:2.272m 7′ 5¼” | W:2.279m 7′ 5 ½” H:2.272m 7′ 5 ¼” | L:11.585m 38″ W:2.162m 7′ 1″ | 4,300 kg 9,480 lbs. | 64.0 cbm 2,260 cu. ft. | 25,181 kg 57,720 lbs |

| 20′ Flat Rack Container | L:5.702m 18′ 8 ½” W:2.438m 8′ H:2.327m 7′ 7½” | 2,330 kg 5,137 lbs. | 28,390 kg 47,773 lbs. | |||

| 40′ Flat Rack Container | L:11.820m 38′ 9 ¼” W:2.184m 7 ½” H:2.095m 6′ 10½” | 5,260 kg 11,596 lbs. | 25,220 kg 55,600 lbs |

Many Importers do not have their own warehousing and distribution services, especially if they have seasonal lows or sporadic activity. Empty warehouses, idle staff and un-utilised vehicles create an un-necessary drain on resources and profitability.

Nucleus PDS offers such services at Heathrow, Barking, Southampton and South Africa.

If you’re interested in learning more about these services please do not hesitate to contact us.

Cargo Insurance is obviously the most reliable and cost effective way to protect a shipper’s cargo against instances of unexpected damage and loss.

Freight forwarders rarely offer their own insurance, however most will be able to recommend a reliable insurance broker.

Please do not hesitate us on details provided should you require any further information on this matter.

In simple terms, a letter of credit is an undertaking by a bank to make a payment to a named beneficiary within a specified time, against the presentation of documents which comply strictly with the terms of the letter of credit.

Its main advantage is providing security to both the exporter and the importer, but the security offered however, comes at a price and must be weighed against the additional costs resulting from bank charges. The exporter must understand the conditional nature of the letter of credit and the fact that payment will not be made unless the terms of the credit are met precisely.

An importer/buyer (Applicant) may open a letter of credit if they wish to ensure that the exporter/seller (Beneficiary) has performed those requirements as per the underlying sales contract, by making the documentation requested conditions of the credit. (N.B. The sales contract is not an inherent part of the letter of credit, although the letter of credit may contain a reference to such contract).

When an exporter asks for payment by letter of credit, he is transferring the risk of non-payment by the buyer to the Issuing Bank -and the Confirming Bank if the letter of credit is confirmed-, providing the exporter presents the required documents in strict compliance with the credit, with the exception of cash in advance. For the exporter a letter of credit is the most secure method of payment in international trade provided the terms of the credit are met.

A bill of lading (also referred to as a BOL or B/L) is a document issued by a carrier e.g. a company’s shipping department, acknowledging that specified goods have been received on board as cargo for conveyance to a named place for delivery to the consignee who is usually identified. A through bill of lading involves the use of at least two different modes of transport from road, rail, air, and sea. The term derives from the noun “bill”, a schedule of costs for services supplied or to be supplied, and from the verb “to lade” which means to load a cargo onto a ship or other form of transport.